In the previous lesson we observed that by

exogenously prohibiting

short-selling a complete

market may become incomplete. This model was the first

example of an incomplete market. In this lesson we will expose an

internal characteristic of the market that can make it incomplete which

does not involve any constraints on the set of trading strategies. As

we mentioned in lesson

8 the models considered so far are one-factor models in the

sense that at any time the price variance can be determined by flipping

one coin because there are only two possible rates of return. We will

see in this section that by allowing more than two rates of return at

anytime the market of module 1 might no longer be complete.

Example: General Motors' (GM) stock, multi-factor

case

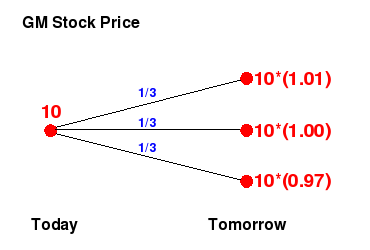

Suppose that GM's stock price behaves as shown in the tree below. On

top of each edge in the tree we have placed the corresponding

probability. Observe that in this case there are three possible rates

of return, either the price goes up by 1%, remains unchanged or goes

down by 3%. Each event can occur with the same probability.

Intuitively, the arbitrage-free condition in this case should remain

invariant, i.e.

d< r< u where,

d,

r and

u are the lowest rate of return,

the interest on the dollar and the highest rate of return,

respectively. Because if this is not the case, there are arbitrage

opportunities like the one presented in example 3 of

lesson

2. Suppose for instance that

r=0. We

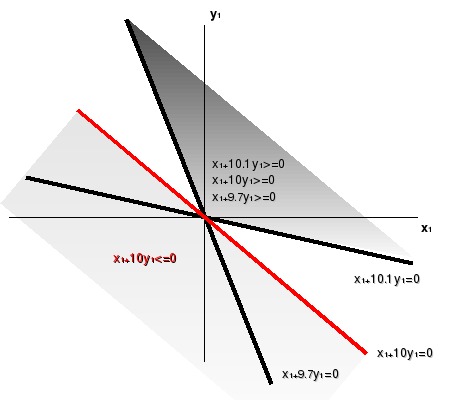

argue as we did in the previous lesson. As shown in the figure below,

the set of trading strategies with nonpositive initial value and the

set of strategies that are nonnegative in the three states of the world

can be represented by a semiplane and a cone, respectively.

The only strategy in the intersection of the semiplane with the cone is

x1=0=y1,

which is not an arbitrage opportunity.

We

leave as an exercise for the reader to check that the same holds when

assuming r to be any value strictly between d=-0.03

and u=0.01. We might ask then,

what is the difference between this

multi-factor model and the one factor model considered in the previous

lessons? The main difference is that under these

hypotheses on the price movement of GM's stock the model is no longer

complete.

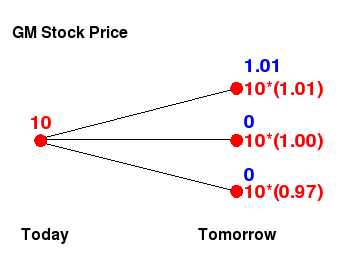

To see this consider a call option with maturity of one day and strike

price equal to 10. The payoffs under the different states of the world

for this option are colored in blue in the tree below.

In order to hedge a position on the call option an investor would

like to find an strategy

(x1,y1)

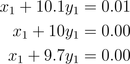

on the money market account and GM stock, respectively. The strategy would solve the

following system of three linear equations in two unknowns (see

lesson

5).

This system has no solution and hence

the

model is not complete. We can also argue that the model is

not complete by using the

second

fundamental theorem of asset pricing. But before doing so we

have to identify what the

martingale

measures are in this model. A probability measure in this

case, can be identified with a triple

(p,q,r) that

specifies the probability of the price going up, staying constant and

going down respectively. Since in our example

r=0,

the martingale property reduces to having expectation equal to 10, i.e.

The other conditions on

p, q and

r

come from the restrictions that they have to be probabilities and hence

p+q+r=1 and since the original

probabilities are all equal to 1/3, in order to have an

equivalent

probability we must require

p,q,r to be

strictly positive. It is easy to see that there exist infinitely many

triples

(p,q,r) that satisfy the conditions above

(some examples are

p=3/5, q=r=1/5 and

p=1/2,

q=1/3, r=1/6) and by the second fundamental theorem of asset

pricing the model is incomplete. It is important to mention that the

fact that there exist at least one triple that satisfies all the

conditions guarantees that the model is arbitrage-free by the

first

fundamental theorem of asset pricing. The same argument can

be used to prove that the model is arbitrage-free if and only if

-0.03=d<

r< u=0.01.

Activity 1

Suppose that the exchange rate between the Euro and dollar today is

€1=$1.5. Tomorrow the price of the Euro either goes up by 10%, stays

constant or goes down by 20%. Each event has the same probability of

occurring. Assuming that the interest rates on the Euro and the dollar

are equal to 0, explain why this model is arbitrage free. Find all the

possible martingale measures for this model and deduce that the model

is incomplete. Give an example of a financial derivative that cannot be

perfectly

hedged in the model.

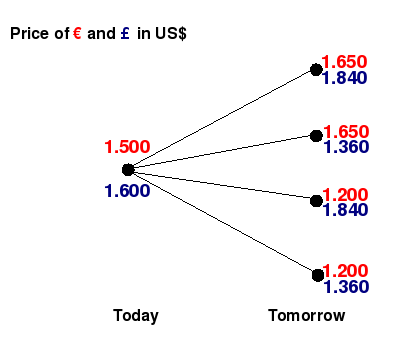

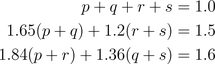

Example: Dollar Vs Euro, Dollar Vs British Pound,

non-correlated case

Recall the example presented at the beginning of

lesson

8. In that model there were only two possible states of the

world either the price of the Euro and pound go up or they go down.

This implies that in our model we are assuming that the dollar price of

the Euro and the British pound are perfectly correlated. By considering

a more general scenario

where the

interest rates on the Euro, dollar and British pound are all equal to 0,

and the correlation hypothesis is dropped we obtain a multi-factor

model. In this model we have four states of the world, which we present

in the tree below. We have added two branches corresponding to the

states of the world in which one price goes up but the other goes down.

In order to find the risk-neutral measures in this model (see

lesson

8), we have to find

(p,q,r,s), strictly

positive numbers such that

It can be shown that there are infinitely many of such quadruples and

hence the market is arbitrage-free but incomplete.

Activity 2

Conduct the same analysis as the one exposed above for the model of

activity 2b) in

lesson

8. In other words study the case when stock's price of

General Motors and Ford are not correlated.

There is a natural extension of the results presented in lessons 7

through 9 to the multi-factor case. We leave this extension as an

exercise for the interested reader.